Updated on November 25, 2025

Written by The Wealthy Gigster Team

Edited by Kevin Nishmas, Managing Editor

At a Glance

Budgeting on irregular gig income is about flexibility, not perfection. Build your budgeting strategy around what you’ve already earned, not what you’re owed. Use weekly cash flow check-ins, smart automation and a solid buffer fund to ride out the chaos. And treat every payout like a mini paycheck by applying the 60/20/20 budgeting rule to cover your essentials, taxes and savings. It’s built specifically for freelancers, independent contractors, self-employed workers, solopreneurs and independent earners who deal with irregular income week to week.

Table of Contents

- Why Don’t Traditional Budgeting Tips Work for Gig Workers?

- What’s the Best Way to Budget on Irregular Gig Income?

- How Can Gig Workers Avoid Going Broke Between Paydays?

- What’s the Best Budgeting Rule for Gig Workers?

- Should I Automate My Budget as a Freelancer?

- Should Gig Workers Track Weekly Cash Flow or Spending?

- Should Gig Workers Budget Weekly or Monthly?

- What’s the Best Way to Manage Bills on Irregular Income?

- How Do I Budget for Unexpected Expenses?

- Should I Separate Business and Personal Accounts?

- What Are the Best Budgeting Apps for Gig Workers?

- Final Thoughts

- Frequently Asked Questions (FAQs)

Key Takeaways

- Budget backwards using what’s already in your account—not what you hope to earn

- Build a buffer fund for feast-and-famine weeks

- Use the 60/20/20 budgeting rule per payout, not monthly

- Automate only what makes sense for irregular income

- Track weekly cash flow, not just spending

- Budget weekly instead of monthly

- Preload your bills to avoid last-minute panic

- Use sinking funds to plan for “unexpected” expenses

- Keep business and personal finances separate

- Use gig-friendly budgeting tools

If you’ve been through the gig grind long enough, you know the idea of budgeting on gig income is about as appealing as a tax audit, unless you’re armed with budgeting tips for gig workers who live pay-to-pay.

For freelancers, independent contractors, self-employed workers, solopreneurs and independent earners living gig to gig, budgeting isn’t about setting the right latte limit. It comes down to surviving the chaos of it all. One week you’re drowning in payouts. The next, all’s quiet on the gig front. Clients ghost you. Work dries up. Your income dwindles faster than your resolve to never dip into your savings—again. And your bills keep piling up.

There’s nothing glamorous about juggling work, invoices and unpredictable paydays that make your bank account go up and down like a roller coaster. Budgeting helps you trade panic for a plan, even when the math still hurts. But if you do it wrong, budgeting on gig income can turn into a full-blown nightmare. You need to apply real-world budgeting tips for gig workers—not conventional “just track your spending” advice that keeps you scrambling for cash.

Why You Can Trust The Wealthy Gigster

We don’t do fluff. And we definitely don’t let advertisers tell us what to say. Every product or service we recommend is vetted using real data, independent research and the financial chaos test: “Would this product or service actually help someone with an irregular income and a rent deadline?”

We rate tools and services based on what matters to gig workers, not 9-to-5ers. If we earn a commission from a partner, you’ll know—but our opinions stay brutally honest, no matter what.

Want the receipts? Check out our About Us, Editorial Standards and Advertising Disclosure pages for how we work and what makes our recommendations worth your time (and money).

Why Don’t Traditional Budgeting Tips Work for Gig Workers?

Conventional budgeting advice assumes you have predictable income. That you can automate your savings. That you can “just set it and forget it.” But that’s not how things work in the gig world. Budgeting tips for gig workers like you only work if they’re built for financial chaos—because your income doesn’t play by the rules.

Most budgeting tips for gig workers like freelancers and independent contractors are written for folks who get paid every other Friday and think budgeting means setting a coffee allowance. These people are not juggling Uber rides, freelance deadlines and random Venmo payments from flaky clients.

For gig workers like self-employed, creative and remote workers, income isn’t predictable. Some weeks you’re up, others you’re eating ramen and praying your payments clear. So, you need budgeting tips for gig workers that flex with your feast-or-famine cycle.

Here are 10 brutally practical budgeting tips for gig workers like you—when you don’t know what or when your next payout will be, but you still want to build wealth and sleep at night.

What’s the Best Way to Budget on Irregular Gig Income?

1. Budget Backwards, Not Forwards

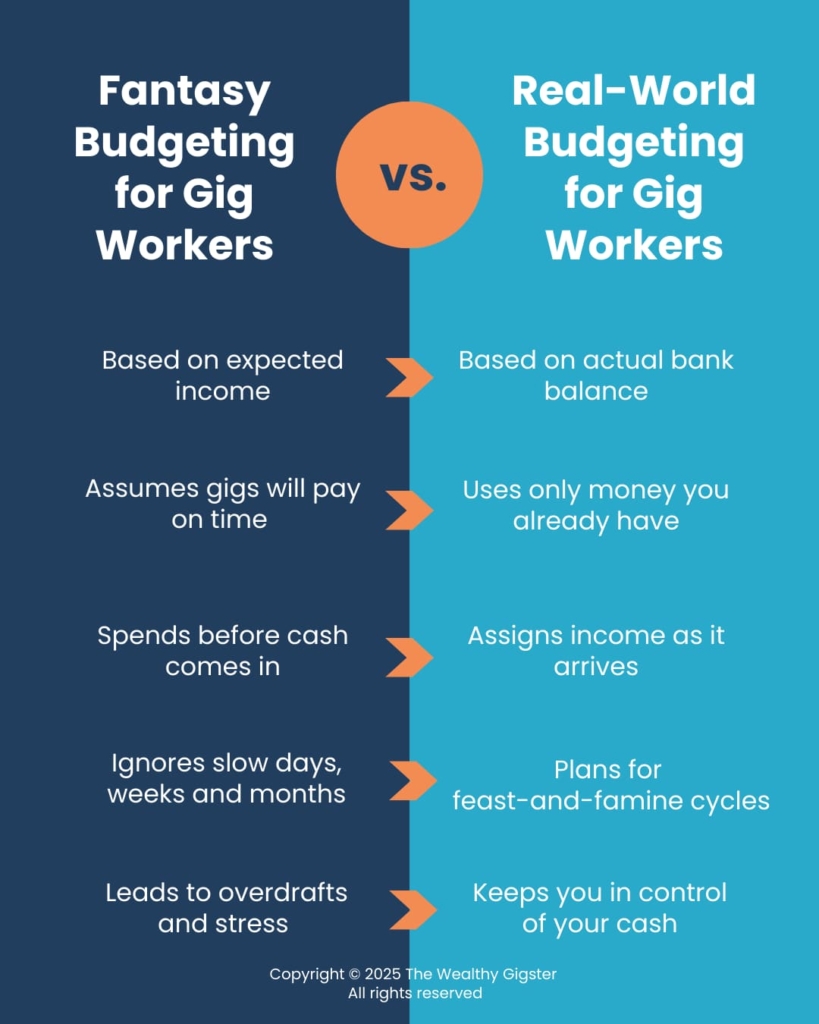

The most effective way to budget on irregular income is to only plan with money you actually have—not money you’re expecting.

Traditional budgeting advice tells you to plan ahead based on how much you think you’ll make each month. But with gig work, guessing your income is like betting on the weather with a dartboard.

Budgeting tips for gig workers like freelancers and independent earners should be based on real cash flow, not wishful thinking.

Budget Based on What’s Already in Your Account

If you have $600 in your account, that’s what you budget—not the $1,200 client invoice that’s been “processing” for two weeks. This keeps you grounded in reality and protects you from spending money you don’t actually have.

Real-World Math: DoorDash Delivery Driver

Let’s say you’re a Dasher and make $120 on Monday, $180 on Wednesday, and $250 on Saturday. Your weekly budget would be $550. Budgeting backwards, you would assign that money to essentials and savings before you even think about extras. This keeps you from overspending based on income you might never earn.

How Can Gig Workers Avoid Going Broke Between Paydays?

2. Build a “Feast and Famine” Buffer Fund

Building a massive emergency fund overnight just isn’t realistic when your income changes from week to week. What you need first is a buffer between your good and slow weeks. This is your “keep the lights on when the gigs dry up” buffer fund.

Building a buffer is one of the most underrated budgeting tips for gig workers like independent contractors and solopreneurs trying to stay afloat between paydays.

To build a buffer fund, stash 10%–20% of each gig payout during your “feast” weeks in a high-yield savings account to earn a high rate of interest. Pick an account that doesn’t come with a debit card or phone app. This makes it much less tempting for you to dip into your buffer fund, even when your client still hasn’t paid you.

But saving is only half the battle. When your income is unpredictable, keeping your savings split between essentials, taxes and goals is just as important. That’s where digital envelopes come in.

Banks call digital envelopes names like vaults, buckets, sub-accounts or pockets, but they all do the same job: letting you split your money in one account to keep your buffer fund, tax reserve and emergency cash separate.

Best High-Yield Accounts with Built-In Digital Envelopes

If you want to build a buffer fund, tax reserve or nest egg without opening multiple accounts, these high-yield savings options can help you divide your money and stay organized.

Minimum Balance: $0

Monthly Fees: $0

Annual Percentage Yield (APY): Up to 3.80% on eligible direct deposits

Digital Envelope Feature: “Vaults” to separate buffer, taxes and savings

More Benefits: Auto-transfer rules and goal tracking in app

Minimum Balance: $0

Monthly Fees: $0

Annual Percentage Yield (APY): 3.60% on any balance

Digital Envelope Feature: Up to 10 “buckets” for different goals

More Benefits: Goal tracking and auto-savings options

Minimum Balance: $0

Monthly Fees: $0

Annual Percentage Yield (APY): 3.70% on any balance

Digital Envelope Feature: Multiple “sub-accounts” for savings goals

More Benefits: Nickname accounts for easy budgeting

Minimum Balance: $0

Monthly Fees: $0

Annual Percentage Yield (APY): 4.00% on any balance

Digital Envelope Feature: Smart goals with assigned contributions

More Benefits: FDIC insured up to $2M and auto allocations

*Rates current as of June 2025. Certain restrictions may apply.

Our Top Pick

SoFi High-Yield Savings checks all the boxes. With this account, you can earn more, stay organized and keep your buffer fund out of arm’s reach—without opening five different accounts.

The Runner-Up

Betterment Cash Reserve is a killer backup, if you want maximum yield with minimal distractions. Just don’t expect to move money in and out instantly.

Bottom Line

Whatever high-yield savings account you choose, even a small buffer fund can help you avoid credit card debt and sleep easier when gig app glitches, clients ghost you or you just need a break from it all.

What’s the Best Budget Rule for Gig Workers?

3. Use the 60/20/20 Budget Rule for Gig Pay

The classic 50/30/20 budgeting rule assumes you have predictable income. You don’t. But you still need a system. Enter the 60/20/20 budget rule for gig workers, including freelancers, online entrepreneurs and creative professionals:

- 60% for essentials (like rent, food and utilities)

- 20% for taxes (a reserve to pay the IRS on time)

- 20% for financial goals (such as building buffer fund, paying off debt or investing)

Apply this rule to every single payout, not just your monthly total. This way, you can stay ahead of the chaos—even when your income is up one week and down the next.

Want to see how the 60/20/20 rule works with your weekly income? Use our free 60/20/20 Budget Calculator to automatically break down your spending and savings every week—with no spreadsheets and no math headaches.

Prefer to plan your budget manually and track your income week by week? Download our free 60/20/20 Budget Worksheet to stay on course, see your spending patterns and spot budget gaps in real time.

Real-World Math: 60/20/20 Budget Rule

Imagine you’re a freelance graphic designer who earns $2,400 one month and just $600 the next. Here’s how the 60/20/20 rule can help you ride out these income swings:

- Month 1 ($2,400): $1,440 (60%) for essentials, $480 (20%) for taxes and $480 (20%) for financial goals.

- Month 2 ($600): $360 (60%) for essentials, $120 (20%) for taxes and $120 (20%) for financial goals.

Bottom Line

By applying the 60/20/20 budget rule during high-income months, you can build a buffer fund that keeps you from panicking the next time a client doesn’t pay on time or gigs dry up.

Don’t knock the 60/20/20 budget rule until you try it—it might be one of the most powerful budgeting tips for gig workers trying to take charge of their finances.

Should I Automate My Budget as a Freelancer?

4. Automate What You Can—Manually Control the Rest

You should only automate certain right parts of your budget. Full automation assumes steady income. You don’t have that. Partial automation gives you both flexibility and control.

Automation is great—until your payment is late and your rent gets auto-deducted from an account that doesn’t have enough money in it.

Because your income changes every week, you need to set smarter rules to maximize the upside of 100% automation (you don’t have to think) and minimize the downside (neither does your bank account). Fortunately, there’s a middle ground that works for gig workers like freelancers, independent contractors and self-employed workers.

Instead of full automation, use “conditional automation”:

- Manually control: Rent, large bills, anything that could overdraft your account.

- Automate: Roundups, small transfers to savings after each deposit and tax fund transfers.

To get the most out of conditional automation, set up rules like “Transfer 15% of any deposit over $100 into savings.” Avoid automatic bill payments from your main account. Use a buffer account or top up your bill accounts ahead of time to avoid nasty surprises.

Tool Tip

Lili lets you automatically transfer a percentage of each deposit into savings buckets—great for taxes, bills, or emergencies. Monarch Money gives you rule-based automation for goals without triggering overdrafts.

Whatever app you choose, stick to manual control for big bills and automate only what you can afford to set and forget.

Should Gig Workers Track Weekly Cash Flow or Spending?

5. Track Weekly Cash Flow—Not Just Spending

Tracking your weekly cash flow is non-negotiable. To stay in control of your money, track what’s coming in, what’s going out and what’s left—every single week.

Tracking your spending is a good start—but it’s not enough to make smart budgeting decisions with unpredictable income. Because you need to budget backwards (remember Tip 1 above), start with what’s due next and decide what’s safe to spend now.

In other words, you should track your weekly cash flow—what’s coming in, what’s going out and what you actually have to spend, save or invest. And it’s easy to do. Just set aside 15 minutes every Sunday to take these steps:

- Add up last week’s income

- List fixed expenses for the coming week

- Estimate variable expenses (such as groceries and gas)

- See what’s left to save, invest or survive on (until your next gig)

Real-World Math: Tracking Cash Flow

For instance, you earn $900 this week. Next week’s rent and bills total $750. That leaves $150. Budgeting backwards, you set aside $100 as a buffer or savings, because next week’s income is unknown. That leaves $50 for groceries or essentials—just enough to get by until more money comes in.

If you had only tracked your spending, you wouldn’t know that $750 needs to be off-limits. You’d see $900 in your account and assume you’re flush—right until rent’s due and you’ve already blown half of it on takeout and a gas refill.

Budgeting backwards stops those last-minute money shocks from happening. It’s one of the most practical budgeting tips for gig workers who don’t have time for surprises.

Tool Tip

To get started, download a simple spreadsheet or use apps like Monarch Money, YNAB, Lili or Goodbudget to log and categorize your weekly cash flow. Not into apps? Even a Google Calendar works—just color-code your cash ins and outs.

Should Gig Workers Budget Weekly or Monthly?

6. Budget Weekly, Not Monthly

Monthly budgeting is basically useless for gig Workers. You can still have monthly goals, but weekly budget tracking gives you a more flexible system.

When your income changes by the gig, budgeting once a month is like checking the weather forecast in a tornado—nice idea, zero help. That’s why you need a weekly budgeting habit.

Instead of trying to predict what the next 30 days will look like, focus on what just happened and what’s coming up in the next seven. It keeps you nimble, alert and in control—even when your paychecks are all over the place.

Here’s how to do it:

- Pick a time—same time every week. Sunday night. Monday morning. Whatever works.

- Look back and ask yourself: “How much did you earn last week?”

- Look forward and ask yourself: “What bills are due this week? Any one-time expenses coming up?”

- Adjust: Do you need to slow your spending? Can you put more toward savings or a sinking fund this week?

Even if it takes just 10–15 minutes, this habit helps you catch issues early (like when a client payment is late) and make smarter, smaller adjustments before things spiral.

Tool Tip

Use a spreadsheet, apps like Monarch Money, YNAB or Goodbudget, or even a Google Calendar with color-coded events. If you can see it, you can stay ahead of it.

Bottom Line

Treat every week like a fresh start, not a financial freefall. Budgeting weekly is one of the budgeting tips for gig workers that you need to stay in control of your finances—no matter how unpredictable the gig economy gets.

What’s the Best Way to Manage Bills on Irregular Income?

7. Preload Your Bills Weekly

Don’t wait until your bills are due. Split them into weekly chunks, so you’re always ahead, not scrambling to pay them.

If you wait for bill due dates to figure out how you’re paying them, you’re already in stress mode. Gig workers don’t get the luxury of stability, so you need to preload your fixed costs before the chaos hits.

Why Preloading Your Bills Work

- You don’t have to scramble on due dates

- You’ll always know your essential expenses are covered

- It helps you spot when your income isn’t keeping pace with your base costs

Real-World Math: Preloading Bills

Let’s say your bills total $1,500 a month. Divide that amount by four weeks ($1,500 ÷ 4 = $375) and aim to stash $375 a week into a separate account or savings bucket just for upcoming bills. When exactly? Every time you get paid.

Tool Tip

To preload your must-pay expenses while the money’s still in your hands, use apps like like Monarch Money, YNAB, Lili or Goodbudget to set aside money for specific bills—like rent, utilities or subscriptions—before you splurge on impulse buys and emergency lattes.

How Do I Budget for Unexpected Expenses?

8. Plan for Unexpected Expenses Like a Boss

Unexpected expenses aren’t accidents—they’re inevitable. You know they’re coming, just not when, so treat them like bills and start saving for them now.

Your tires blow out. One of your subscriptions renews without warning. Your laptop dies mid-project and takes everything you’ve done—and your sanity—with it.. These aren’t surprises—they’re eventuals. And that’s exactly why planning for “unexpected” expenses is non-negotiable.

Where do you start? Set up sinking funds—mini savings buckets for future expenses you know are coming, but like to play peekaboo with your with your bank balance. With these funds, you’re not saving just in case. You’re saving because it’s only a matter of time.

Because your income is unpredictable, you can’t afford surprise expenses. Sinking funds can help you smooth out irregular costs, stay out of debt and make future-you less broke and more chill.

Start by building up sinking funds for the usual suspects:

- Car repairs and maintenance

- Tech upgrades (because your laptop isn’t immortal)

- Healthcare and dental work

- Subscriptions and business tools

- Holiday gifts, birthdays and other joyfully expensive events

Even if you’re only dropping $10 a week into each sinking fund, it adds up. That slow drip turns into a safety net. When that $300 bill smacks you out of nowhere, you won’t have to put it on a credit card or skip meals to cover it.

Real-World Math: Unexpected Expenses

- Month 1: You earn $1,800. You need $600 for a car repair in 6 months, so you set aside $100 per month. That leaves you with $1,700 to cover your regular expenses this month.

- Month 2: You earn $800. You’ll need $400 for a new phone in 4 months, so you set aside $100 per month. That leaves you with $700 for your other monthly needs.

Tool Tip

Apps like YNAB, Monarch Money, Lili and Goodbudget let you set categorized savings goals, so you can label your sinking funds and track your progress—without needing a spreadsheet or sacrificing your soul to formulas and formatting.

Should I Separate Business and Personal Accounts?

9. Separate Your Gig Income From Your Personal Spending

Mixing your gig income with personal expenses is the fastest way to miss write-offs, skip paying yourself and panic at tax time.

Instead, create a dedicated business account. Next, stash all your client payments, app payouts or gig deposits there. Then, transfer only what you need for personal bills.

Ask anyone who’s been through it: the moment your first big expense hits or tax time comes around, you’ll be very glad your gig income isn’t tangled with your grocery bill.

The benefits?

- It’s easier to calculate your profits

- It’s simpler to budget (and save)

- It leads to less tax-time chaos

Try this idea to make this budgeting tip work for you: Transfer a flat amount (for example, $500/week) to your personal account every Monday. Boom—your own version of a paycheck.

Tool Tip

Lili lets you categorize business expenses, save for taxes and invoice from one place.

What Are the Best Budgeting Apps for Gig Workers?

10. Use Gig-Friendly Budgeting Tools

You need tools that adapt to non-traditional income—because budgeting apps built for 9-to-5ers won’t cut it when your paydays are random.

Most budgeting apps are built for people with predictable paydays. You’re not that person. Instead, look for apps that can do these tasks for you:

- Track every individual payout

- Let you create custom pay periods

- Help you bucket money for taxes and savings

- Easily tag income and expenses by client or gig

Avoid apps that only show monthly averages. That’ll just mess with your head if you had a high-earning week followed by a $0 stretch.

Tool Tip

If you’re juggling unpredictable paydays, you need a budgeting app that actually understands the chaos. The apps below are built for gig workers like freelancers, solopreneurs and digital nomads who don’t get paid on a set schedule.

Whether you need to track income per deposit, separate business and personal finances, automate tax savings or build sinking funds, these tools help you stay one step ahead of your money.

Why It Works for Gig Workers: Built-in flexibility for variable income

Key Features: Sync accounts, custom budget periods, goal tracking and visual savings buckets

Why It Works for Gig Workers: Assigns every dollar a job as you earn

Key Features: Envelope-style budgeting, real-time syncing and weekly planning tools

Why It Works for Gig Workers: A budgeting tool purpose-built for freelancers and gig workers

Key Features: Auto-categorized business expenses, tax-saving buckets, invoicing and early pay

Why It Works for Gig Workers: Envelope-style budgeting with hands-on control over every dollar

Key Features: Simple cash-style categories (good for low-income or no-frills budgeting)

Choosing the right budgeting tool isn’t just a convenience. It’s how you turn budgeting tips for gig workers into real financial progress—fast—whether you’re a solopreneur, freelancer or independent app earner.

Which App Should You Choose?

- Monarch Money → Best for full-featured budgeting and goal planning

- YNAB → Ideal if you want total control and don’t mind a learning curve

- Lili → Great if you want banking + budgeting in one app (especially for freelancers)

- Goodbudget → Simple, old-school envelope budgeting if you like manual tracking

Final Thoughts

Budgeting isn’t about cutting your caffeine habit or feeling guilty for ordering Uber Eats. It’s about control. It’s about having a system in place before chaos hits.

A good gig budget lets you take breaks without a financial panic attack, say no to sketchy clients because you’re not desperate, and handle dry spells with a buffer—not a meltdown.

You don’t need consistent income to build wealth. You just need budgeting tips for gig workers that were built for unpredictability, not perfection. This way, you will have a solid budgeting system that flows with your hustle.

Frequently Asked Questions (FAQs)

How do gig workers budget with unpredictable income?

Start by budgeting only the money that’s already in your account. Use the 60/20/20 rule per payout (60% essentials, 20% taxes, 20% savings/goals), and build a buffer during high-earning weeks to smooth out lean ones. These are some of the most reliable budgeting tips for gig workers, like freelancers, independent contractors and solopreneurs, looking to manage unpredictable income.

What is the best budgeting method for gig workers?

A weekly cash flow approach combined with per-payment budgeting is best. You track what comes in and goes out each week, rather than relying on monthly predictions that don’t reflect income volatility. This method is especially effective when budgeting for freelancers who manage multiple gigs at once. It’s one of the budgeting tips for gig workers that adapts to real income patterns—not fixed paydays.

Are there budgeting apps designed for gig workers?

Yes. Tools like Monarch Money and Lili offer features like per-deposit tracking, tax buckets and flexible planning options that are ideal for freelancers and gig workers. These tools are designed to help you manage irregular income with less stress—making them perfect companions to the budgeting tips for gig workers shared in this post.

How do I save for taxes if I get paid irregularly?

Use a separate savings account and set aside 15%-25% of every gig payout as soon as you receive it. Automating this with conditional transfers can prevent end-of-year tax surprises.

What should gig workers include in a budget?

As a gig worker, you should include essentials like rent, groceries and transportation, plus savings goals, tax reserves and irregular expenses like healthcare or equipment. Also, don’t forget to plan for slow periods and emergencies. These are the kinds of budget categories that the most important budgeting tips for gig workers focus on—especially if you’re trying to keep things stable when your income goes up and down.

How can I manage inconsistent income without feeling broke all the time?

Build a gig survival fund, preload your bills and separate business and personal accounts. These habits reduce stress and make your money easier to manage, even when gigs are a hit or miss.

What’s the easiest budgeting tip for gig workers just starting out?

Start with budgeting backwards. Instead of guessing what you might earn this month, build your budget around what’s already in your account. It’s simple, realistic and one of the most effective budgeting tips for gig workers who need to make smart money decisions fast—especially when paydays are unpredictable.

How often should gig workers review their budget?

Weekly is best. When your income changes by the job, a monthly check-in just doesn’t cut it. Set aside 15 minutes each week to review your earnings, upcoming bills and spending. It’s one of the most practical budgeting tips for gig workers who want to stay in control without getting overwhelmed.

How can I avoid spending money I should be saving as a gig worker?

Use sinking funds and separate accounts. Setting aside small amounts for specific goals—like taxes, tech upgrades or emergencies—helps you resist the urge to spend what looks like “extra” cash. This is one of the budgeting tips for gig workers that turns good intentions into real financial protection.