Updated on November 25, 2025

Written by The Wealthy Gigster Team

Edited by Kevin Nishmas, Managing Editor

At a Glance

The 60/20/20 budget for gig workers gives you a simple, adaptable budgeting approach to follow: 60% of your income goes to essentials, 20% to taxes and 20% to your financial goals. Unlike traditional monthly budgets, this one works weekly, making it ideal for freelancers, independent contractors, solopreneurs and other self-employed workers who live with irregular income—because it can be adjusted week by week. Once you understand how to use this gig-friendly budgeting strategy, you’ll stop fearing cash flow gaps and start making your money work for you.

Table of Contents

- Key Takeaways

- Why Do Gig Workers Need a 60/20/20 Budgeting Strategy?

- What Is the 60/20/20 Rule—And How Is It Different?

- Should Gig Workers Budget Weekly Instead of Monthly?

- What Belongs in Your 60% “Essentials” Bucket?

- Why Should You Always Carve Out 20% for Taxes?

- How Should You Use the Final 20% to Build the Future You Want?

- Download Your Free 60/20/20 Budget Worksheet Template

- How Do You Automate Your 60/20/20 Budget?

- How Do You Handle Budget Blowups Without Ditching the 60/20/20 Rule?

- What If Your Income Is Too Low for The 60/20/20 Budget Strategy?

- What is the Best Time to Review and Adjust Your 60/20/20 Budget?

- What are Common Mistakes Gig Workers Make with the 60/20/20 Budget Rule?

- Final Thoughts

- Frequently Asked Questions (FAQs)

Key Takeaways

- The 60/20/20 budget for gig workers breaks your after-tax income into three easy buckets (60% essentials, 20% taxes, 20% financial goals).

- This strategy works for freelancers, independent contractors, solopreneurs and independent earners, not just app-based earners.

- This weekly budgeting approach is ideal for gig workers who don’t earn steady income (since you can just recalculate your 60/20/20 percentages based on what you made that week).

- The 60/20/20 Budget Worksheet Template helps you see exactly where your money should go (and where you might be overspending) on a week-by-week basis.

- Taxes are non-negotiable (budget for them like your financial well-being depends on it, because it does).

- The final 20% is where you build the life you actually want (it’s how you go from just getting by to finally getting ahead).

Why Do Gig Workers Need the 60/20/20 Budget Rule?

Traditional budgets weren’t built for gig life or self-employed income. They assume you receive a predictable paycheck, work the same hours each week and rely on built-in benefits like health insurance and a retirement plan, which gig workers just don’t have.

When your income swings every which way like a busted screen door in the wind, trying to fit your finances into a rigid, one-size-fits-all monthly budget is like squeezing into jeans from your teenage years. It’s uncomfortable and unsustainable.

Without a budget that adapts to the week in, week out changes in your freelance income, you end up in survival mode. Constantly reacting. Dreading slow weeks. Burning through savings (if you have any left).

Enter the 60/20/20 budget rule: a flexible, adaptable budgeting system that adjusts to the unpredictable ups and downs of your gig income weekly—and puts you back in control.

Why You Can Trust The Wealthy Gigster

We don’t do fluff. And we definitely don’t let advertisers tell us what to say. Every product or service we recommend is vetted using real data, independent research and the financial chaos test: “Would this product or service actually help someone with an irregular income and a rent deadline?”

We rate tools and services based on what matters to gig workers, not 9-to-5ers. If we earn a commission from a partner, you’ll know—but our opinions stay brutally honest, no matter what.

Want the receipts? Check out our About Us, Editorial Standards and Advertising Disclosure pages for how we work and what makes our recommendations worth your time (and money).

What Is the 60/20/20 Budget Rule—And How Is It Different?

The 60/20/20 budget for gig workers is a weekly plan that adapts to your income—not the other way around.

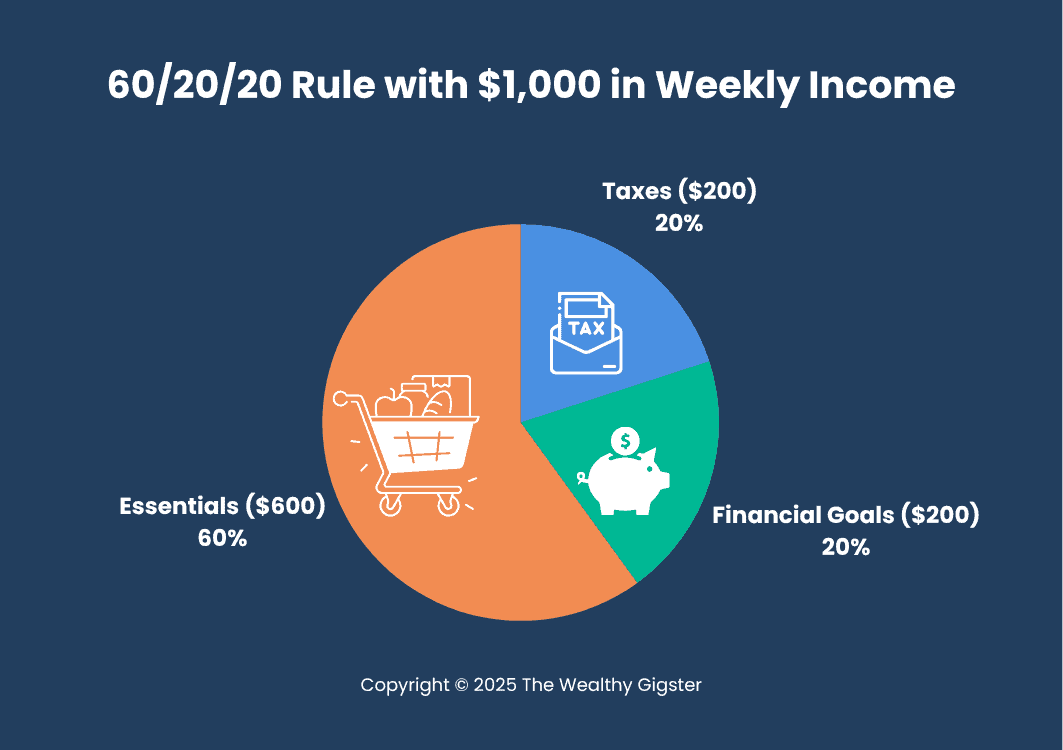

The 60/20/20 rule splits your net (after-tax) income into three clear percentages:

- 60% for essentials: rent, food, gas, utilities and work gear

- 20% for taxes: income tax, self-employment tax and state taxes

- 20% for financial goals: savings, retirement and investments

Instead of itemizing every last coffee, you zoom out. You get a bird’s-eye view of where your money should be going or where you’re overspending—and you track your cash flow in broad strokes.

Real-World Math: The 60/20/20 Budget for Gig Workers in Action

If you make $1,000 this week:

Should Gig Workers Budget Weekly Instead of Monthly?

Yes, weekly budgeting makes the irregular cash flow of most gig workers much more manageable and far less terrifying. It’s also a solid budget approach for freelancers, digital nomads and independent creators juggling multiple clients or earning platforms.

Waiting until month-end to figure out if you’ve made enough income is a recipe for anxiety. Budgeting by week keeps you agile. It lets you adapt your budget in real time. There’s no guesswork, no last-minute panic.

Freelancers often earn income from multiple sources (like Uber, Etsy, Fivver and Upwork). A weekly structure lets you rebalance your cash flow regularly, instead of relying on guesstimates.

Real-World Math: Budgeting on Fluctuating Weekly Income

Because the 60/20/20 budget for gig workers is percentage-based, it flexes with your income. No matter how much you earn, you always know how to split it—and avoid that dreaded “Oops, I overspent” spiral.

Let’s say your income fluctuates week to week:

Week 1: You earn $450

- 60% ($270) → Essentials (rent, food, transportation)

- 20% ($90) → Taxes (self-employment, state, federal)

- 20% ($90) → Financial goals (debt repayment, savings, investing)

Week 2: You earn $950

- 60% ($570) → Essentials (maybe extra groceries, a utility bill)

- 20% ($190) → Taxes (more income = higher withholding)

- 20% ($190) → Financial goals (bigger payment toward credit cards or emergency fund)

What Belongs in Your 60% “Essentials” Bucket?

Your essentials category should include your bare-minimum expenses to live and work. Think rent, food, health care and everything else you can’t ghost without consequences.

“Essentials” include your housing, food, transportation, phone, insurance, childcare and utilities. For gig workers like self-employed workers, online entrepreneurs and freelancers, essentials also include work tools that keep you earning, like software, data and equipment.

This is not the time to fudge the numbers. Essentials = what keeps you employed, sheltered and alive. It’s different for everyone, but it’s got to be an honest calculation.

Real-World Math: Weekly “Essentials” Breakdown

Let’s say your weekly income is $1,200. Using the 60/20/20 rule, here’s how you should split your earnings for the week:

- 60% = $720 for essentials

- 20% = $240 for taxes

- 20% = $240 for financial goals

Now let’s break down the essentials category:

- Rent: $400/week (if paid weekly)

- Groceries: $100/week

- Phone bill: $50/week

- Gas: $70/week

- Car insurance: $50/week

Total spent on essentials: $670

That leaves you with $50 left in your essentials bucket. You can:

- Use it as a buffer for surprise expenses (like an oil change)

- Pay a small bill (such as a subscription or minimum credit card payment)

- Roll it into next week if you know a bigger cost is coming

The beauty of this system? You always know what’s safe to spend—and what’s already spoken for.

Why Should You Always Carve Out 20% for Taxes?

One of the easiest traps to fall into is not setting aside enough cash to pay Uncle Sam when tax season arrives. For gig workers like freelancers, solopreneurs and independent contractors, carving out 20% from every gig payout for taxes is the simplest way to avoid a nasty surprise when Uncle Same comes to collect.

If you don’t plan for taxes, they’ll ambush you like a surprise bill at tax time. Because you don’t have a traditional job, your paychecks don’t automatically withhold taxes. That means you’ve got to be your own accountant. You need figure out how much to have in your bank account to pay your taxes on time.

The 20% tax bucket ensures you’re ready to pay your income tax, self-employment tax, sales tax, state taxes, even random stuff like vehicle or carbon tax. It’s your built-in reminder to keep the tax man off your back and out of your savings because, let’s face it, the government never forgets, even when you do.

And planning ahead isn’t optional for gig workers when it comes to taxes. It’s essential. A 2025 survey from Avalara found that 74% of gig workers can’t identify the IRS 1099‑K income threshold, and many end up scrambling at year‑end to figure out what they owe.

When you carve out that 20% weekly, you shield yourself from penalties, stress and having your bank account hit hard around tax time.

Real-World Math: 20% “Tax” Bucket

Let’s say you earn $800 from gigs this week. Using the 60/20/20 budget budget for gig workers, $160 (20% of $800) should go straight to your tax bucket. Here’s how that $160 breaks down (roughly):

- Self-employment tax (12%) = $96

- Federal and state income tax (6%) = $48

- Buffer for unexpected taxes (2%) = $16

By setting aside $160 immediately:

- You won’t be caught off guard when the IRS asks for their cut

- You avoid draining your emergency fund to cover taxes

- You may even end up with extra left over (for a small splurge)

Even better, move that $160 to a high-yield savings account labeled “Do Not Touch (Tax Money).” Automate the transfer if you can. You’ll thank yourself during tax season when everyone else is stressing out.

How Should You Use the Final 20% to Build the Future You Want?

For solopreneurs, freelancers and digital nomads, the final 20% bucket for financial goals is your freedom fund. Don’t waste it. The last 20% of the 60/20/20 budget for gig workers isn’t for blowing on impulse buys. It’s for building your future, your way. That means paying down debt, investing in IRAs, creating an emergency fund or saving for a down payment.

This 20% gives you breathing room. It gradually turns your feast-or-famine gig income into financial stability and control. Some weeks you’ll only save $40. Others, $400. That’s fine—as long as you consistently set aside 20% for your most important financial goals every week.

The Everee 2025 Gig Driver Report looked into financial coping strategies among 419 U.S. gig drivers (Uber, DoorDash, Shipt). The key takeaways:

- 59% relied on gig work for at least half their income

- 65% had taken payday loans due to delayed gig earnings

- 61% postponed essential purchases when pay was slow

Translation: When your income is unpredictable, you’re essentially walking a financial tightrope—without a safety net. Budgeting methods like the 60/20/20 budget rule transform those highs and lows into predictable, manageable amounts.

Real-World Math: 20% “Financial Goals” Bucket

Let’s say you earn $1,000 this week. With the 60/20/20 budget for gig workers, the final 20%—aka your “financial goals” bucket—is $200 for building your future (not just surviving today). Here’s how you might break it down:

- $100 to your emergency fund – For when your car dies, your gig app glitches or life throws something stupid at you. Every deposit brings you closer to sleeping soundly through the next crisis.

- $50 to your investment account – Could be a micro-investing app like SoFi or Acorns. The point? Start now—even small amounts grow if you keep showing up weekly.

- $50 toward credit card debt – Not glamorous, but important. Tackling it little by little helps reduce interest and keeps you from sinking when your gig income dips again.

This is how that final 20% can take you from paycheck-to-paycheck to actually making financial progress. Even when you’re not earning big, you’re still moving forward to the future you want to live.

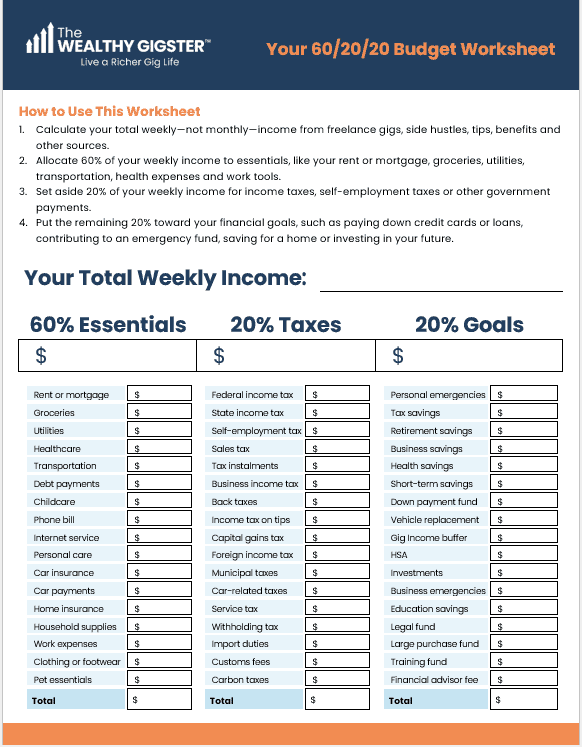

Download Your Free 60/20/20 Budget Worksheet Template

Budgeting advice means nothing if you don’t know where your money is going. Using a 60/20/20 budget worksheet can help you track your income and spending, stay accountable and make smarter decisions week by week.

To get started, download our free 60/20/20 Budget Worksheet for Gig Workers, a no-nonsense, easy-to-use tool designed to help you apply the 60/20/20 rule week by week—with line-by-line suggestions for what counts in each category.

How to Use the 60/20/20 Budget Worksheet

Start by entering your total weekly income from all your gigs, side hustles, tips and benefits. Next, allocate that amount to three categories:

- 60% for essentials (like groceries, rent, phone bill, gas)

- 20% for taxes (such as federal tax, state tax, self-employment tax and sales tax)

- 20% for financial goals (like debt repayment, savings or investing in future-you)

Each category comes with a detailed list of example expenses—so you’re never left wondering what “essentials” or “goals” actually mean in your life. It gives you room to track what you earn, how you spend and where to pivot—one week at a time.

Want to finally see where your money should go (and where it’s slipping through the cracks)? Here’s a preview of a downloadable worksheet that can keep your weekly budget real—and you in control.

Click here to download your free worksheet and start budgeting weekly.

The 60/20/20 worksheet is a solid starting point—especially if you’re a pen-and-paper type or just learning how to budget weekly. But once you get the hang of things, it’s worth leveling up to budgeting tools that do the heavy lifting for you.

Want to see exactly how to split your weekly income using the 60/20/20 budget for gig workers? Try our free 60/20/20 Budget Calculator to automatically (and instantly) find out how much to set aside for essentials, taxes and savings—no spreadsheets and no stress necessary.

How Do You Automate Your 60/20/20 Budget?

Set up automatic transfers: 60% to checking for bills, 20% to a separate tax account and 20% to a savings or investment account. Most online banks or apps make this easy. Set it once. Forget it. Let your budget run in the background while you do literally anything else.

The less you have to think about moving money, the more consistent you’ll be with your 60/20/20 budget. Even better, apps and automation tools can save you time and help you track, tweak and stay on top of your money with way less effort.

Whether you’re trying to keep taxes in check, hit savings goals or finally make your budgeting stick, these gig-friendly tools can do the heavy lifting while you focus on earning.

Best Budgeting Apps for Gig Workers: Manual + Weekly-Friendly

If you’re juggling multiple income streams and irregular paychecks, you need a budgeting app that’s built for your reality—not your accountant’s. These apps make it easier to track your weekly income, separate your essentials from your wants and stick to the 60/20/20 budget for gig workers without breaking into a spreadsheet-induced panic.

Best for: Hands-on budgeters who want total control over weekly income and goals

Why We Like It: It’s built around giving every dollar a job—perfect for applying the 60/20/20 rule on a weekly basis.

Tool Details: Works across devices, syncs accounts and focuses on aging your money and forecasting expenses.

Best for: Couples or solo users who want sleek visuals and detailed tracking

Why We Like It: Its dashboard gives a clean, instant snapshot of spending, making it easy to compare income vs. goals.

Tool Details: Provides bank syncing, customizable dashboards and long-term planning tools.

Best for: Tracking real-time cash flow and spending trends

Why We Like It: It’s easy to see where your money is going, and it adapts well to weekly or fluctuating incomes.

Tool Details: Automatically categorizes income and expenses, tracks cash flow in real time and offers forecasting.

Best for: Quick-glance spenders who need a “safe to spend” number

Why We Like It: It strips budgeting down to the basics and keeps you from blowing through your essentials.

Tool Details: Connects to accounts, analyzes bills and spending, and recommends budget tweaks.

Best for: Freelancers, independent earners and the self-employed who need accountability and don’t mind some sass

Why We Like It: It uses AI (and humor) to make budgeting more engaging and surprisingly helpful.

Tool Details: Includes a budgeting assistant via chat, sends spending alerts, tracks trends and savings goals.

Best for: Fans of zero-based budgeting who are disciplined weekly planners

Why We Like It: It’s a solid app if you’re ready to plan every dollar manually—just not as flexible as others.

Tool Details: Requires hands-on setup and tracking (based on Dave Ramsey’s zero-based budgeting method).

Our Top Pick: YNAB (You Need A Budget)

If you want a budgeting app that helps you plan weekly, stick to the 60/20/20 rule and actually stay consistent, YNAB is your best bet. It’s hands-on, flexible, and built for gig workers who want to take control.

Runner-Up: Monarch Money

For a more visual, intuitive experience—especially if you’re budgeting with a partner—Monarch Money is a sleek alternative that still gets the job done without overwhelming you with too much detail.

Best Tools for Automating Savings + Transfers: Set It and Forget It

These tools help you move your money automatically—so the 20% buckets for your financial goals and taxes fill up without needing manual transfers, reminders or willpower. Each one is tailored to make sticking to your 60/20/20 budget smarter and easier.

Best for: Rule-based automation with total customization

Why We Like It: It lets you set creative savings rules that align perfectly with weekly income habits.

Tool Details: Creates savings triggers based on spending, round-ups, goals, or even specific days of the week.

Best for: Freelancers who need hands-off savings for taxes and benefits

Why We Like It: It’s built specifically for gig workers, and makes saving for taxes feel painless.

Tool Details: Automatically withholds a certain percentage from each deposit for taxes, retirement, and even paid time off.

Best for: Simple auto-savers who want to earn interest too

Why We Like It: It offers basic automation and competitive interest rates—great for beginner savers.

Tool Details: Sets up recurring weekly transfers and rounds up savings from purchases into a high-yield savings account.

Best for: Remote workers who want smart savings and financial guidance

Why We Like It: It uses automation and real human advice to help you save, invest and improve your finances without lifting a finger.

Tool Details: Offers auto-savings based on your income and spending habits, plus access to real financial advisors and investing options.

Our Top Pick: Qapital

If you want to make saving money for goals or taxes feel effortless (and kind of fun), Qapital is your go-to budgeting tool. It lets you set up custom rules—like rounding up every coffee purchase or saving $10 every time you say “I’ll start Monday.”

Runner-Up: Catch

Built specifically for freelancers, Catch helps you save for taxes, time off, retirement and health expenses—all from the same paycheck. Just connect your bank account, set your percentages and it’ll do the rest, before you can spend anything.

Best Tools for Tax Budgeting & Withholding

These tools help gig workers automatically separate and manage taxes before they’re accidentally spent. Whether you’re juggling multiple income streams or trying to stay ahead of quarterly payments, these apps make tax budgeting far less stressful.

Best for: Self-employed gig workers who want one tool to track income, expenses and taxes

Why We Like It: It combines everything you need—tax tracking, invoicing, mileage logging and clean reporting—all on one dashboard.

Tool Details: Links to your bank, auto-categorizes expenses and gives you quarterly tax estimates, so you’re never surprised.

Best for: Small business freelancers who want banking + tax organization

Why We Like It: It uses budgeting buckets and easy tax tracking to keep your money organized without extra effort.

Tool Details: Provides virtual envelopes for taxes, expenses and goals, plus integrates with Stripe, QuickBooks and other freelancer tools.

Our Top Pick: QuickBooks Self-Employed

If you want an all-in-one tax solution that works as hard as you do, QuickBooks Self-Employed is your best bet. It tracks income, expenses, mileage and invoices—plus it gives you reliable estimates, so you’re not blindsided at tax time.

Best for Passive or Micro-Investing

When you’re ready to move beyond budgeting and start growing your money, these tools make it easy. Whether you’re investing spare change or setting up weekly auto-deposits, these apps let you build wealth passively—no spreadsheets or financial jargon required.

Best for: Gig workers who want flexible investing with perks and no management fees

Why We Like It: It offers both automated and DIY investing, plus extras like free financial planning and career coaching.

Tool Details: No account minimums, zero management fees for automated investing and access to goal-based portfolios or individual stocks.

Best for: Set-it-and-forget-it savers who want to invest spare change with minimal effort

Why We Like It: turns small purchases into long-term investments, making it perfect for gig workers who want to invest in the background.

Tool Details: Automatically rounds up transactions and invests the difference in diversified portfolios based on your goals.

Our Top Pick: SoFi Invest

If you’re looking for a flexible investing platform that does more than just grow your money, SoFi Invest is your go-to tool. It offers automated portfolios, DIY investing and bonus perks like financial planning and career coaching—great for gig workers who want more than just returns.

How Do You Handle Budget Blowups Without Ditching the 60/20/20 Rule?

Bad weeks happen. That doesn’t make you bad at budgeting—it makes you human. What matters is how you bounce back. Here’s how to do it.

Let’s say a surprise vet bill nukes your “goals” fund or your “essentials” creep into the “tax” zone. Don’t panic. Don’t toss the whole plan. The 60/20/20 budget for gig workers is a strategy, not a cage.

Start by triaging the damage: Where did the overspend happen? What category took the hit? Then course-correct. Maybe next week, your essentials stay lean while your savings bucket gets a refill.

This method thrives on momentum. Breaks are fine. Just don’t let them become your new default.

Think of it like a GPS: when you veer off course, it doesn’t shame you—it just reroutes. The 60/20/20 rule does the same. It gives you a flexible path forward, not a punishment. One blown week doesn’t erase your progress; it just gives you better data for the next one.

What If Your Income Is Too Low for The 60/20/20 Budget Strategy?

You tweak your 60/20/20 budget system. You don’t trash it. Progress isn’t about perfect ratios. It’s about consistency and awareness.

If 60% of your income barely covers groceries, rent and gas, you’re not failing—your math just needs adjusting. You could try 70/10/20 (if taxes are lower), 80/10/10 (if you’re in survival mode), or even just start by tracking where anything is going for two weeks.

At the end of the day, of course, it doesn’t matter if it’s 60/20/20 or 75/15/10 or whatever—as long as you’ve got a budget plan that helps you stop bleeding cash. Whether it’s 60/20/20 or a close cousin, the act of budgeting brings clarity. You’ll spot leaks faster, prioritize what matters, and stop the slow drip of spending that sabotages your goals—even with a modest income.

Think of it like resizing a jacket. If it doesn’t fit right now, you tailor it. The key is to keep using the 60/20/20 budget framework, even if you have to bend the rules for a while. Life gets easier when you have numbers guiding your next move instead of vibes.

When is the Best Time to Review and Adjust Your 60/20/20 Budget?

Your money habits need check-ins—just like your relationships. We recommend doing a quick review at the end of every week. Look at what you earned, what you spent and what you saved. If you’re seeing red in one category, adjust before it spirals.

Monthly reviews are great for zooming out, spotting patterns and refining your goals. But weekly is where the real-time wins happen. That’s when you catch overspending before it snowballs, adjust for lower-than-expected income or reallocate your categories on the fly.

Your weekly check-ins are how you stay grounded, course-correct quickly and stay engaged with your money in a way that feels manageable, not overwhelming.

Set a Sunday night calendar reminder with your favorite beverage in hand. Call it your “Budget + Beverage Ritual.” Whatever works for you. Make it a habit you actually look forward to.

What are Common Mistakes Gig Workers Make with the 60/20/20 Budget Rule?

Most budgeting fails come down to three avoidable mistakes: miscounting income, misusing goal money and skipping your weekly check-ins.

The top offender? Counting gross income instead of net. You’ll feel rich on payday—until tax season shows up with an attitude. When you budget like you get to keep every dollar, you set yourself up for an ugly surprise. Always start from what’s actually yours to spend.

Another biggie? Treating the 20% “goals” slice like fun money. It’s tempting—especially after a big deposit—to blow that chunk on something shiny. But that 20% is where your future lives: your savings, debt payoff, investments, your shot at freedom. Letting it become “whatever money” is how short-term pleasure eats long-term progress.

And then there’s the silent killer: skipping the weekly check-in. One missed review turns into two, and before you know it, you’re back to winging it. That’s how budgets die—quietly, in the background, while your spending goes rogue.

The fixes?

- Set up a separate tax savings account and automate transfers, so you don’t “accidentally” spend what’s not yours.

- Label your categories in plain English (not “Miscellaneous 2” or “Budget Stuff”), so you know exactly what’s what.

- Stay consistent—even if you flub a week. Progress isn’t lost in the misstep. It’s lost when you don’t get back on track.

Final Thoughts

Budgeting doesn’t have to be complicated or soul-crushing—especially when you work gigs for a living.

The 60/20/20 budget rule for gig workers is all about creating a system that fits your gig life—without all the stress that comes with it. When you use a percentage-based approach, you stop chasing the perfect budget and start making real financial progress. It gives you boundaries. Flexibility. Confidence.

You don’t need to master every financial app or memorize tax codes. You just need to know how much is coming in and where it should go. So give it a shot. Use the worksheet. Try one of the apps.

Start this week. And remember: small moves made consistently can lead to big financial wins.

Frequently Asked Questions (FAQs)

How do gig workers budget with unpredictable income?

Start by budgeting only the money that’s already in your account. Use the 60/20/20 budget rule for gig workers per payout (60% essentials, 20% taxes, 20% savings/goals), and build a buffer during high-earning weeks to smooth out lean ones. These are some of the most reliable budgeting tips for gig workers looking to manage unpredictable income.

What is the best budgeting method for gig workers?

A weekly cash flow approach combined with per-payment budgeting is best. You track what comes in and goes out each week, rather than relying on monthly predictions that don’t reflect income volatility. This method is especially effective when budgeting for freelancers who manage multiple gigs at the same time. It’s one of the budgeting tips for gig workers that adapts to real income patterns—not fixed paydays.

Are there budgeting apps designed for gig workers?

Yes. Tools like Monarch Money and Lili offer features like per-deposit tracking, tax buckets and flexible planning options that are ideal for freelancers and gig workers. These tools are designed to help you manage irregular income with less stress—making them perfect companions to the budgeting tips for gig workers shared in this post.

How do I save for taxes if I get paid irregularly?

Use a separate savings account and set aside 15%-25% of every gig payout as soon as you receive it. Automating this with conditional transfers can prevent end-of-year tax surprises.

What should gig workers include in a budget?

As a gig worker, you should include essentials like rent, groceries and transportation, plus savings goals, tax reserves and irregular expenses like healthcare or equipment. Also, don’t forget to plan for slow periods and emergencies. These are the kinds of budget categories that the most important budgeting tips for gig workers focus on—especially if you’re trying to keep things stable when your income goes up and down.

How can I manage inconsistent income without feeling broke all the time?

Build a gig survival fund, preload your bills and separate business and personal accounts. These habits reduce stress and make your money easier to manage, even when gigs are a hit or miss.

What’s the easiest budgeting tip for gig workers just starting out?

Start with budgeting backwards. Instead of guessing what you might earn this month, build your budget around what’s already in your account. It’s simple, realistic and one of the most effective budgeting tips for gig workers who need to make smart money decisions fast—especially when paydays are unpredictable.

How often should gig workers review their budget?

Weekly is best. When your income changes by the job, a monthly check-in just doesn’t cut it. Set aside 15 minutes each week to review your earnings, upcoming bills and spending. It’s one of the most practical budgeting tips for gig workers who want to stay in control without getting overwhelmed.

Get free gig money advice.

Because you earned it.

Sign up for our newsletter and get the free gig money advice you need to live a richer gig life.

By subscribing to our newsletter, you acknowledge and agree to our Terms of Use and Privacy Policy. You can unsubscribe at any time.

Featured Image by TheStandingDesk on Unsplash